How Rising Interest Rates Affect Investors

Written by The Content Team

Published on October 25, 2018

minute read

Share:

The Bank of Canada raised its benchmark interest rate again on Wednesday, citing a solid outlook for the global economy and reduced uncertainty around trade thanks to the new U.S.-Mexico-Canada Agreement (USMCA).

The key rate now stands at 1.75 per cent, up from 1.50 per cent most recently, marking the fifth rate hike since last summer.

The rate, officially known as the target for the overnight rate or the policy interest rate, dictates the interest rate at which banks borrow and loan money between each other overnight. It's closely watched since it's a strong indicator as to where other interest rates are headed, like those for mortgages and consumer loans.

When the Bank of Canada raises its overnight target rate, what it's really aiming to do is slow down borrowing and spending to keep inflation in check.

What does an interest rate hike mean for investors? Here are a few considerations:

Fixed Income

The fixed-income family includes many types of investments, including bonds, treasury bills, bankers' acceptances, guaranteed investment certificates (GICs) and mortgage-backed securities. Here we'll focus on bonds to show the possible impact of rising interest rates.

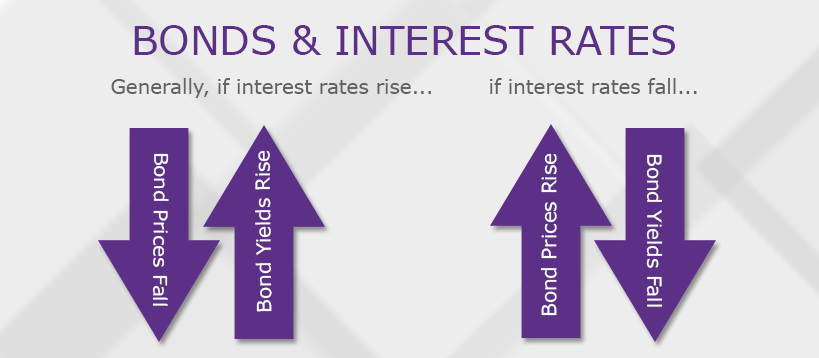

When markets start to anticipate an increase in rates, bond yields can head higher.

Interest rate moves can be challenging for bonds as the price of bonds tends to have an inverse relationship with interest rates. As one of a few factors that bonds are sensitive to (inflation risk and credit risk are others), interest rate risk refers to the risk of rising interest rates and a reduction in the market value of a bond. Why does this happen? A bond's price may fall to reflect its lower coupon rate relative to comparable bonds issued more recently at higher rates. At the same time as its price declines, the bond's yield moves higher, keeping it competitive in the market.

While the price of existing bonds may drop as rates rise, interest income could benefit if reinvested at a higher rate. Existing bonds in the market might also be available at higher yields, or new bonds may be issued with more attractive coupons.

Keep In Mind

- Holding a bond until it matures means fluctuations in its market price would have less impact on the holder. That's because interest payments are predictable over the life of the bond, and the principle would likely be paid out upon maturity, providing the issuer doesn't default.

- While fixed-income returns may come under pressure in the short-term, a strategic allocation to fixed income is still considered by many to be a key ingredient in a well-diversified portfolio.

Stocks

Traditional thinking is that rising interest rates create headwinds for equities. There are a few reasons behind this point of view:

- Higher rates can mean higher borrowing costs for companies, which risks impacting their return on capital.

- Higher rates can sometimes make more secure, interest-bearing instruments like bonds more attractive to investors, which may result in lower demand for stocks.

- Higher rates may mean companies spend more to service debt and less on capital investments, which may affect future earnings growth.

But…

It's important to keep in mind the reasons behind interest-rate hikes. When the Bank of Canada moved off the sidelines in 2017, it cited in part a robust economy, including strong employment. For companies, a strong economy can help drive corporate earnings.

Margin Accounts

Have a margin account? In keeping with the recent rise in the cost of borrowing, interest rates on margin loans have increased. This means that you have to pay more to leverage (or borrow) against your existing investments.

What about currencies and interest rates? Read 5 Takeaways on Interest Rates & Foreign Exchange.

RBC Direct Investing Inc. and Royal Bank of Canada are separate corporate entities which are affiliated. RBC Direct Investing Inc. is a wholly owned subsidiary of Royal Bank of Canada and is a Member of the Canadian Investment Regulatory Organization and the Canadian Investor Protection Fund. Royal Bank of Canada and certain of its issuers are related to RBC Direct Investing Inc. RBC Direct Investing Inc. does not provide investment advice or recommendations regarding the purchase or sale of any securities. Investors are responsible for their own investment decisions. RBC Direct Investing is a business name used by RBC Direct Investing Inc. ® / ™ Trademark(s) of Royal Bank of Canada. RBC and Royal Bank are registered trademarks of Royal Bank of Canada. Used under licence.

© Royal Bank of Canada 2025.

Any information, opinions or views provided in this document, including hyperlinks to the RBC Direct Investing Inc. website or the websites of its affiliates or third parties, are for your general information only, and are not intended to provide legal, investment, financial, accounting, tax or other professional advice. While information presented is believed to be factual and current, its accuracy is not guaranteed and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author(s) as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by RBC Direct Investing Inc. or its affiliates. You should consult with your advisor before taking any action based upon the information contained in this document.

Furthermore, the products, services and securities referred to in this publication are only available in Canada and other jurisdictions where they may be legally offered for sale. Information available on the RBC Direct Investing website is intended for access by residents of Canada only, and should not be accessed from any jurisdiction outside Canada.

Explore More

AI Stocks: Making Sense of the Market Swings

What exactly is happening in the AI sector and how can investors make sense of it all?

minute read

7 Ways to Get Ahead Financially in 2026

How you might invigorate your finances and put your money to work more intentionally this year

minute read

Economic Outlook: Uncertainty is Here to Stay, So What's Next?

Takeaways from the Economic Club of Canada’s Annual Event

minute read

Inspired Investor brings you personal stories, timely information and expert insights to empower your investment decisions. Visit About Us to find out more.